IDCFP’s Early Warning Signal Forecasts A Potential Banking Crisis in 2021

Brokers of CDs and investors in CDs, as well as insurance companies, federal agencies, state governments, interbank lending, and a host of other institutions rely on IDC Financial Publishing’s (IDCFP’s) CAMEL rankings to make better business decisions. Our unique and proprietary methodology provides early warning signs of the next potential banking crisis.

This article summarizes the components of CAMEL, and how this approach is used to forecast the next banking crisis. Similar to the period of growing bank risk seen in 2005-2006, which signaled the crisis of 2008-2009, we are witnessing a growing number of institutions ranked below 125, or below investment grade, with our CAMEL analysis.

The Seeds of a Problem

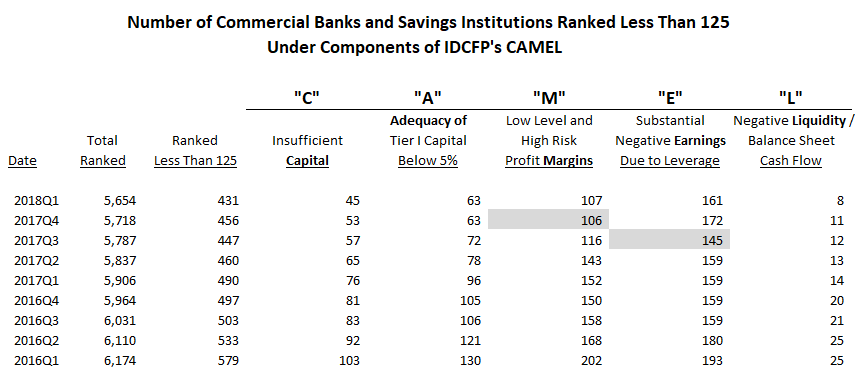

Although the total number of banks ranked less than 125 by IDCFP continues to decline, components of the CAMEL rating are exhibiting characteristics of a change in direction. As shown in Table I column “E,” more banks began exhibiting negative returns on financial leverage (ROFL*) in 2017 Q4. In addition, there was a small increase in institutions yielding narrow profit margins with high standard deviations in this margin over time, shown in column “M.”

*ROFL = operating returns on earning assets minus the cost of funding as a percent of adjusted debt (both after tax) multiplied by leverage.

The other 3 components of IDCFP’s CAMEL are still declining or holding, indicating some time before a full reversal. “C” or number of institutions with capital that is deemed insufficient is still declining, currently at 45. “A” or institutions measuring adequate Tier 1 Capital adjusted for loan delinquency did not change from the previous quarter. Finally, “L” or institutions with negative liquidity in balance sheet cash flow is also still declining, currently at a level of 8 institutions (see Table I).

Table I

The Effect of Rising Interest Rates in a Strong Economy

The Federal Reserve raised interest rates twice in 2018 to a decade high of 2%. The Fed is expected to increase rates 2 more times in 2018 and up to 4 times in 2019, depending upon the strength of the economy and new lows in unemployment.

Banks with low after-tax operating profit returns, due to inefficiencies in operations, experience the same increase in funding costs as other banks. A low return from operations, combined with rising funding costs, creates a negative leverage spread. This negative spread multiplied by a bank’s leverage provides a highly negative return on financial leverage, leading to more banks ranked below 125 due to the “E” component in CAMEL.

Banks have operated in a low interest rate environment for many years. For profit margins to remain strong or increase, banks are required to charge higher loan rates to compensate for the rise in funding costs. However, without a 10-year T-Note yield of 4-5% in coming years, banks will be limited in their ability to raise interest rates on loans.

Loan delinquency primarily impacts the "A" and "L" in IDCFP's CAMEL rating, keeping these components repressed. However, following a robust economy in 2018, 2019 or 2020, a recession in the housing market is possible in 2021. With bank lending highly focused on home loans, bank loan delinquencies could accelerate as a result. IDCFP monitors the Housing Market Index, which measures home buying confidence and traffic, and uses this index as a leading indicator of a housing downturn and potential rise in home loan delinquencies.

History of Early Warning Indicators

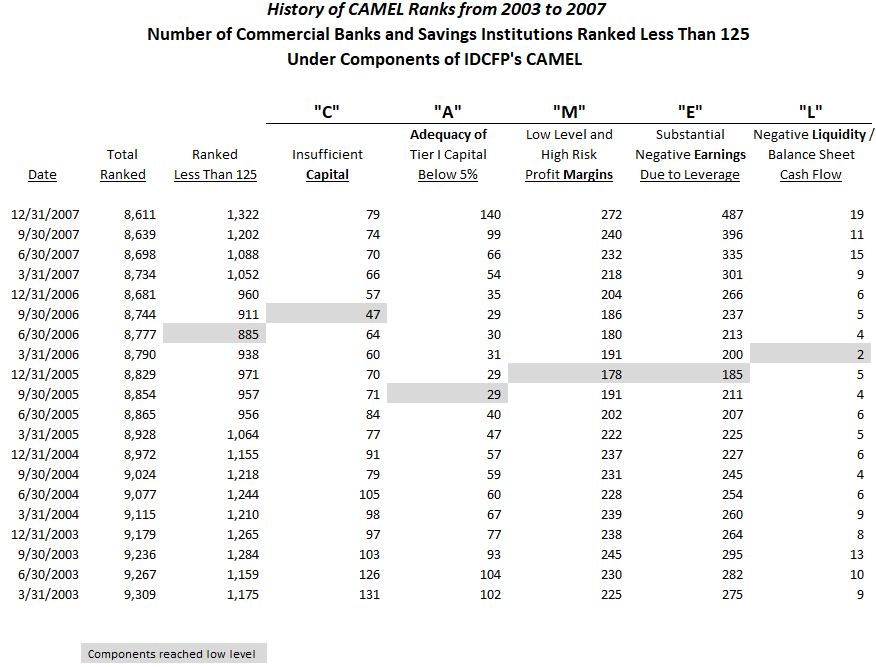

The number of commercial banks and savings institutions ranked below 125 reached a low in the 2nd quarter of 2006, two years before the banking crisis in 2008. More importantly, leading up to this point, 4 out of the 5 components of CAMEL also reached lows from the 3rd quarter of 2005 through the 1st quarter of 2006, and then began to rise.

As seen in Table II below, commercial banks and savings institutions with insufficient capital reached a low of 47 institutions in the 3rd quarter of 2006. Financial institutions measuring adequate Tier 1 capital, adjusted for delinquency below 5%, reached a low count of 29 in the 3rd quarter of 2005. Banks and savings institutions with a lack of profitability, or low and unstable margins, reached a low of 178 in the 4th quarter of 2005. The commercial banks and savings institutions with severe negative earnings due to leverage reached their low of 185 in the 4th quarter of 2005. Finally, institutions with high loan delinquency and negative balance sheet cash flow, or negative liquidity reached their low of 2 in the 1st quarter of 2006.

Additionally, in June 2005 the Housing Market Index peaked, and then declined for the remainder of that year. In 2006, the HMI declined significantly further, confirming a housing recession and rise of bank loan delinquencies.

Table II

As seen in history, the increase in the number of financial institutions with IDCFP’s CAMEL ranks below 125, or below investment grade, forecast the bank financial crisis years later. IDCFP’s ranks are critical for investors to monitor financial institutions.

For further information or to view our products and services please feel free to visit our website at www.idcfp.com or contact us at 800-525-5457 or info@idcfp.com.

John E Rickmeier, CFA

President

Robin Rickmeier

Marketing Director

IDC Financial Publishing, Inc.

700 Walnut Ridge Drive, Suite 201

PO Box 140

Hartland, WI 53029

P 800-525-5457

P 262-367-7231

F 262-367-6497